Atlas Global Equity Income – Monthly Manager Commentary

February 2026

During February we initiated a new position in BHP, the world’s largest copper producer. We also purchased Costco, a best-in-class, low-cost retailer of everyday products. To make way for these new holdings, we exited our positions in Automatic Data Processing and Euronext.

Both Brambles and Fastenal announced robust dividend increases, of 21% and 11% respectively, during the month.

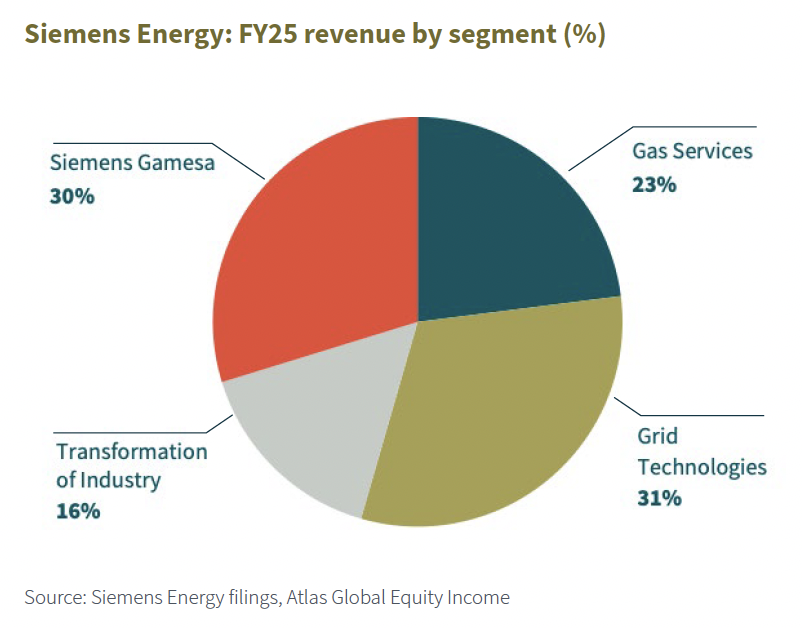

Featured holding – Siemens Energy

This month we highlight Siemens Energy, which was spun off from Siemens AG in 2020 as part of a strategy to carve out its mature energy assets. Siemens would refocus on high-growth areas like factory automation, intelligent buildings and rail transport solutions, while the less fashionable Siemens Energy, with its gas turbines, transformers and turbines, would become an independent “energy pure play”.

The company’s early days of independence were brutal. They were marked by persistent net losses from FY20 through FY23, driven largely by challenges at the business’s wind unit, Siemens Gamesa. However, these challenges overshadowed progress in other segments, foremost among them Grid Technologies and Gas Services.

Surging global electricity demand from electrification trends, particularly AI/data centre expansion, is driving increasing sales of grid-related products like transformers and inverters. Additionally, gas turbine demand, which had been in the doldrums in the run-up to the spin-off, rebounded strongly post spin-off, supported by hyperscalers circumventing the grid altogether and deploying onsite gas-fuelled power right next to their data centres.

This demand allowed Siemens Energy to post its first profit as an independent company in FY24, reporting net income of €1.34 billion. FY25 was even better, with net income of €1.69 billion. Due to AI’s relentless need for electricity, Siemens Energy has found itself a key player in the AI/data centre buildout.

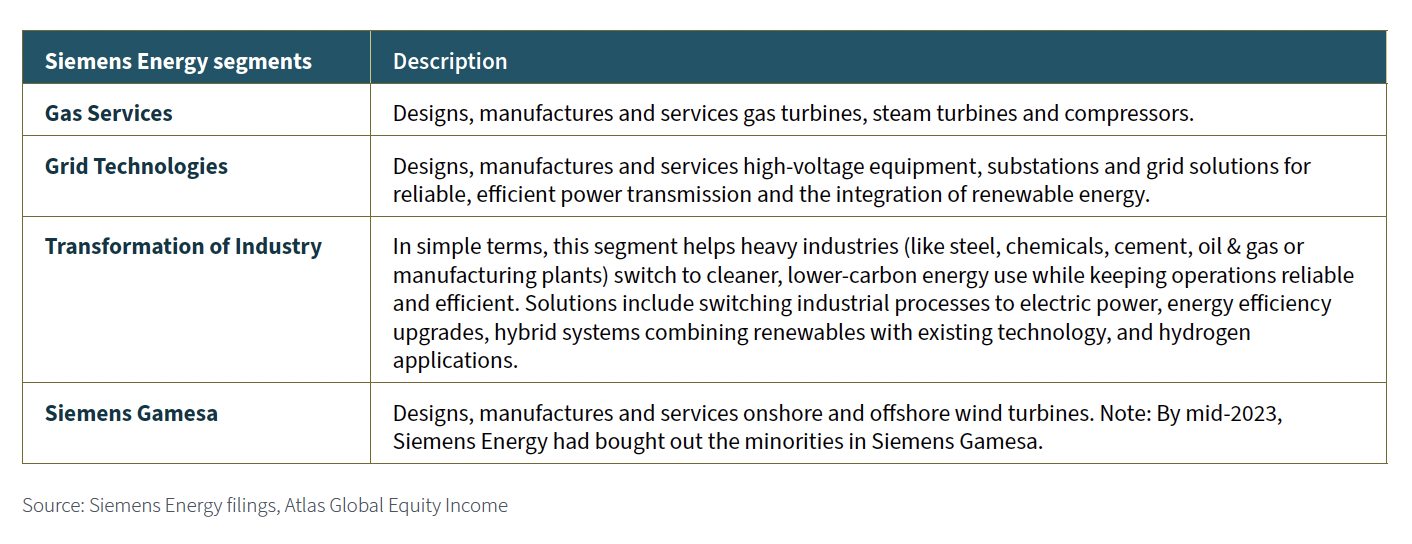

Siemens Energy segments

Before we dive deeper, let’s look at Siemens Energy’s four segments.

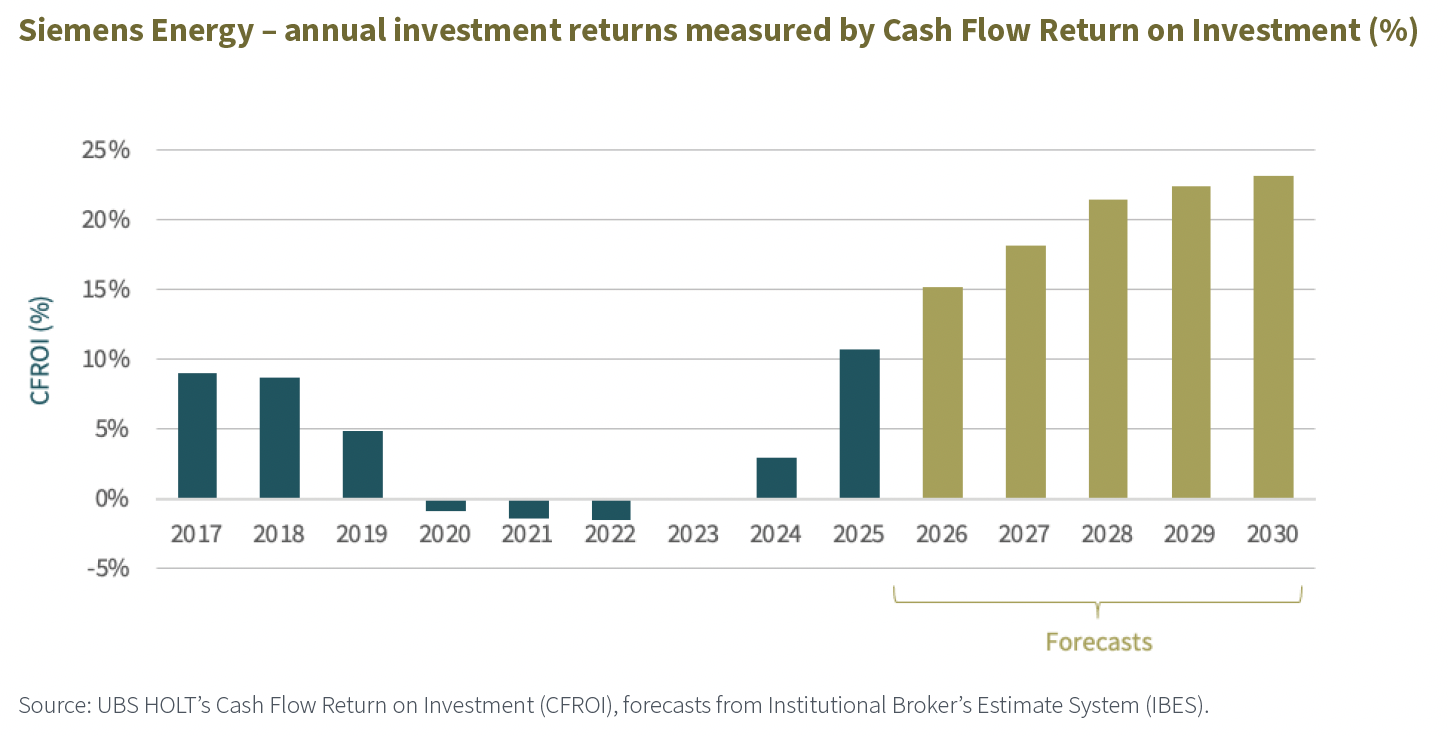

In the wilderness

As mentioned above, the years between 2020 and 2023 did not go according to plan. Return on investment, as measured by HOLT’s Cash Flow Return on Investment (CFROI) metric, showed negative returns in 2020, 2021 and 2022 and was zero in 2023 (see chart on page 3). This poor performance was largely caused by restructuring costs, impairment charges and the impact of COVID-19 – and then the wind turbine problems started.

The wind turbine troubles – Siemens Gamesa

Siemens Energy first flagged problems at Siemens Gamesa in early 2023. Some of the wind turbines were failing. The company announced charges for the unit of €472 million, which “were triggered by an evaluation of the failure rate of the installed fleet, during which Siemens Gamesa detected a negative development of failure rates in specific components, resulting in higher warranty and service maintenance costs than previously estimated”.

Worse was to come. On June 23 2023, referring to its wind turbine unit, Siemens Energy announced: “The current status of the technical review suggests that in order to reach the targeted product quality of certain Onshore platforms, significantly higher costs will be incurred than previously assumed. Potential quality-related measures and the associated costs are currently under evaluation and are likely to be in excess of €1 billion.”

Note how the finger was pointed at the onshore turbine business. In the same announcement Siemens Energy withdrew FY23 profit guidance. The shares dropped -37% that day.

The German government eventually had to step in to guarantee loans and allow management to unpick the mess.

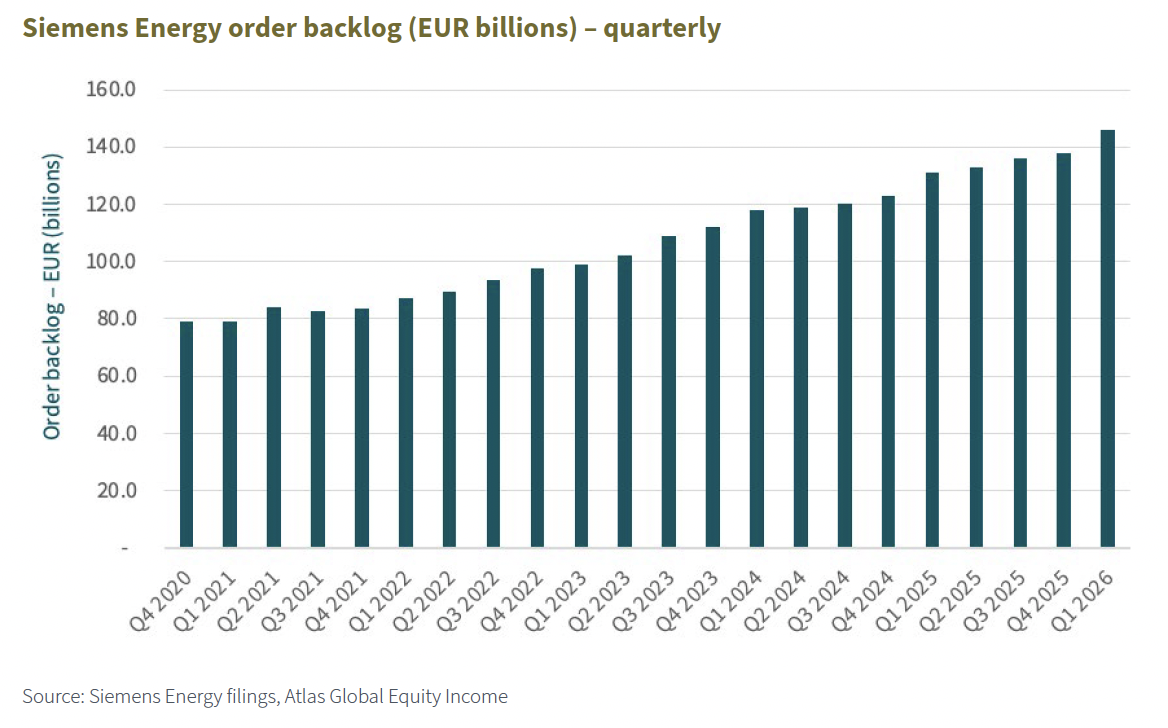

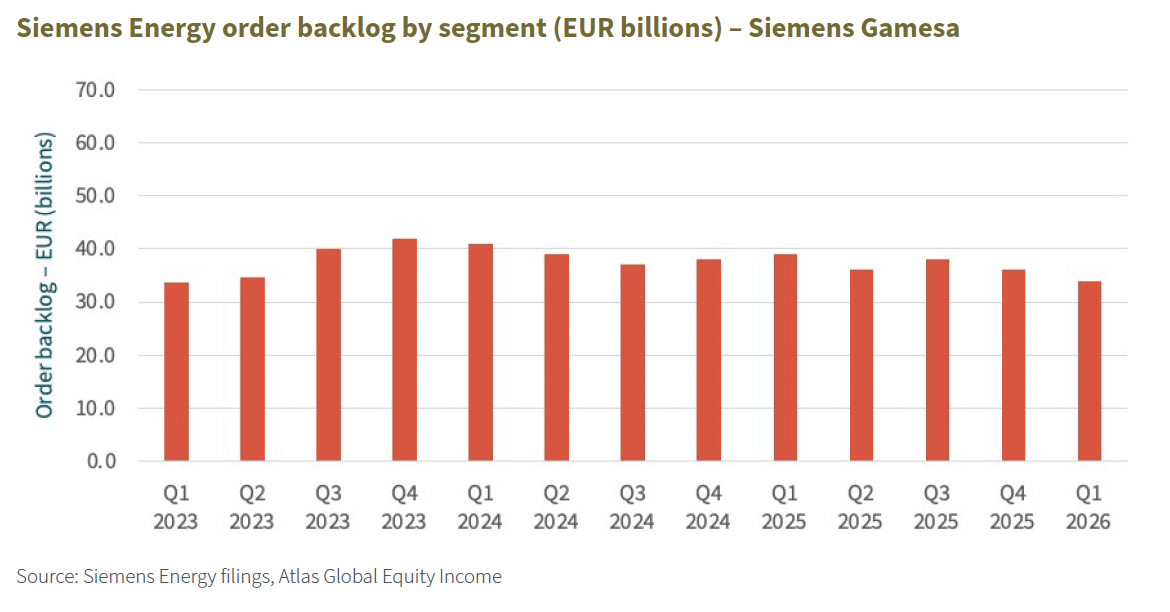

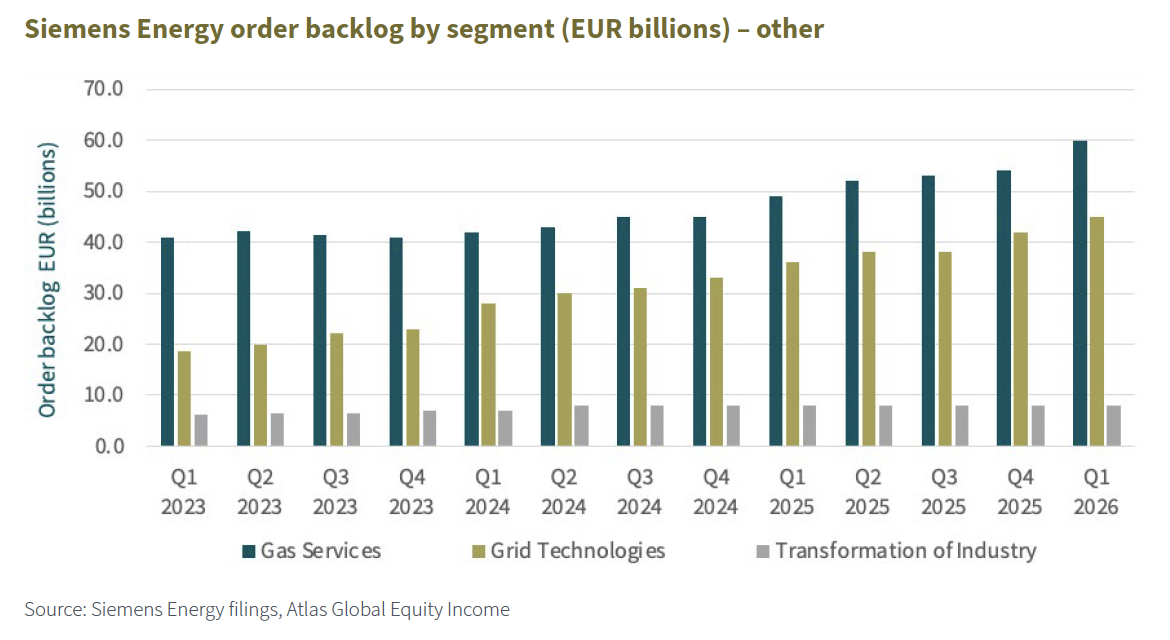

Order backlog

Profitability, return on investment and the share price told a miserable story in those early years of independence, yet the company’s order backlog told a different tale. Group order backlog has nearly doubled in five years.

Segment reporting changed at the beginning of 2023, so it is not possible to compare each segment to Q4 2020. However, a look at the order backlog by reporting segment gives an insight into what was driving the increase.

As would be expected, Siemens Gamesa’s order backlog stagnated following the turbine issues. It remains at 2023 levels.

However, Grid Technologies and Gas Services have shown exceptional growth over the same period.

Grid Technologies

Siemens Energy’s Grid Technologies division designs, manufactures and services high-voltage power transmission and distribution equipment. It provides solutions like transformers, inverters, switchgear (e.g. circuit breakers), High Voltage Direct Current (HVDC) systems, FACTS (Flexible AC Transmission System) devices, substations and smart grid technologies.

Key drivers of Grid Technologies sales

Political support

International initiatives such as the Paris Agreement and sovereign state legislation are supporting a trend towards decarbonisation. Electrification, combined with the replacement of fossil fuels, helps with this objective.

Integrating renewable energy with the grid

The move towards renewables has also driven demand for grid-related products. This is where we need to get a little technical, but don’t worry – it won’t get too involved.

Utility-scale wind turbines produce alternating current (AC) electricity. However, because of fluctuating wind speeds, the power is variable in both voltage and frequency. To make it compatible with the electricity grid, voltages and frequencies need to be matched.

A power converter within the turbine first converts the variable AC to direct current (DC) and then inverts it back to AC, matching the grid’s exact specifications.

A step-up transformer, typically located at the turbine’s base, then cranks up the voltage significantly – for example, from around 690 V to about 33 kV – to minimise energy losses during transmission. This is because higher voltages are much more efficient at power transmission than lower voltages. The electricity then travels through underground or overhead cables to a central substation, where power from multiple turbines is gathered and combined. At the substation, another transformer increases the voltage to even higher transmission levels – between 110 kV and 400 kV – before the power is fed into the main high-voltage grid for delivery to homes, businesses and industries.

Large solar farms, on the other hand, use photovoltaic panels to generate direct current (DC) electricity, which varies with the amount of sunlight. Power inverters are used to convert this variable DC to stable alternating current (AC), synchronised to the grid’s frequency. Step-up transformers then raise the voltage, typically from about 400-800 V to 33 kV, again to reduce transmission losses. The AC power travels via cables to a central substation, where additional transformers increase voltages to higher transmission levels (110-400 kV), before being fed into the main high-voltage grid for delivery to consumers.

In short: the rise of renewable power brings a whole range of challenges to connect this power to the grid. As a result, it requires increasing amounts of equipment (e.g. transformers, inverters, etc.) to manage this integration. Siemens Energy’s Grid Technologies segment offers products and services for exactly this type of work.

Three offshore transformer modules waiting to be deployed at the Moray East Offshore Wind Farm. Image: Siemens Energy

Data centres

According to Goldman Sachs, data centres accounted for roughly 3-4% of total US electricity demand in 2023. They are expected to reach 8% of total US electricity demand by 2030.

The four largest US hyperscalers – Alphabet, Amazon, Meta and Microsoft – are projecting a combined $625 billion of capex spend in 2026. The majority of this spend will be directed towards data centre buildout. It is therefore easy to see how Goldman Sachs’ 2030 forecast could become reality.

Behind-the-meter strategies

Hyperscalers are increasingly turning to on-site power generation by building their own electricity generation right next to their data centres. Known as a “behind-the-meter” strategy, this approach helps avoid major grid bottlenecks and long interconnection delays – which are often between four and seven years or even lengthier in some high-demand areas. Waiting on the grid simply slows down hyperscalers’ expansion plans.

The bridge fuel

Seen as the cleanest of fossil fuels, electricity production using gas turbines and natural gas is increasingly viewed as a pragmatic solution to immediate power needs – one that avoids coal and oil. This is why it is often described as a “bridge” fuel for the energy transition.

In addition, gas-fired plants can ramp up or down quickly, often in minutes, providing backup for intermittent renewables like wind and solar and so adding a much-needed layer of reliability.

Gas Services

Prior to Siemens Energy’s spin-off from Siemens AG, large gas turbine sales suffered a 35% drop in sales compared with FY15 levels. A little context is important here.

2015 was the year of the Paris Agreement, the first legally binding global climate treaty. Hydrocarbons were on notice. Exactly 30 months later, in a May 2018 presentation, Siemens management bluntly stated there were “no signs of recovery” on the mid-term horizon.

After the spin-off, however, gas turbine sales did start to recover. In 2024 and 2025, as hyperscalers increasingly considered behind-the-meter strategies, they began to accelerate. The segment sold a hundred gas turbines in FY24 and 194 in FY25. Siemens Energy booked 102 gas turbines in Q1 2026 alone.

Siemens Energy CEO Christian Bruch directly addressed the topic of gas turbine delivery times during the company’s first earnings call of 2026, held on February 11. He said: “Our delivery times continue to increase, and this is simply the fact of the matter. We’re talking about the delivery dates [for] 2029 and 2030. There were some slots for 2028, but [it’s] a very high-demand market.”

The International Energy Agency’s Energy for AI report, released last April, noted: “Grid congestion and connection queues are growing in many regions, and supply chains for key components like transformers and gas turbines are stretched. In our analysis and modelling of these factors, we estimate that around 20% of the projected data centre additions by 2030 in our Base Case could be at risk of delay.”

With Siemens Energy’s Grid Technologies and Gas Services segments seeing such high demand, the Agency’s prediction seems to have some sound logic.

A gas turbine rotor at a high-speed balancing facility. Image: Siemens Energy

Wind turbines – Siemens Gamesa

But what about Siemens Energy’s problematic segment, Siemens Gamesa? As mentioned previously, FY23 was a difficult year: the wind segment reported losses of €4.3 billion before special items, while the other segments posted profits. Siemens Gamesa continued to post losses before special items in both FY24 (losses of €1.8 billion) and FY25 (losses of €1.4 billion).

Siemens Energy has implemented a comprehensive turnaround plan for the wind unit to restore it to profitability. First, it needed to resolve the onshore turbine quality issues through design fixes and retrofits to reduce future warranty costs. It also needed to get wiser about bidding for contracts. Remarkably, some legacy contracts had no inflation protection clauses, leading to losses.

In November 2025, at its Capital Markets Day, Siemens Gamesa outlined a slimmed-down onshore future with fewer platforms, target markets and factories. It also highlighted offshore driving growth and ramping up its “workhorse” 15 MW platform, with high installation rates planned for FY26-27.

These efforts appear to be making progress. In Q1 2026 losses stood at €46 million – a notable improvement – with the unit forecast to break even in FY26.

While the unit has been a serious drag on group financial performance for the past few years, improvements are being made. In addition, the future for wind energy remains bright. The International Energy Agency projects wind power will continue to play a key role in the energy transition, accounting for 30% of global renewable electricity growth through 2030. Wind-based generation is forecast to nearly double, to over 2,000 GW, by the end of the decade, surpassing hydropower to become the second-largest renewable source.

Westermost Rough Offshore Wind Power Plant. Image: Siemens Energy

Conclusion

Siemens Energy has encountered challenges, most notably with its wind turbine unit, since being spun out of Siemens AG in 2020. Financial performance between 2020 and 2023 was poor. Yet disappointing results have masked a strong order backlog and high demand in the company’s Grid Technologies and Gas Services segments.

Artificial intelligence and the data centre buildout are now driving increased demand for electricity. This surge has fuelled record order intake, particularly in gas turbines and grid-related equipment such as transformers. The company’s order backlog has risen to a record €146 billion in Q1 2026, profits have nearly tripled, and there are early signs of stabilisation in the business’s wind operations. As a result, we believe Siemens Energy is well-positioned for long-term growth and improved profitability in the coming years, capitalising on the global energy transition and AI-driven power needs.

Michael Foster, Fund Manager and Roger Breuer, Analyst – Atlas Global Equity Income

February 2026

Disclaimer:

As at the end of February 2026, Atlas Global Equity Income holds a long position in Siemens Energy. This article is not to be taken as investment advice.

………………………

| AUTHORISED AND REGULATED BY THE FINANCIAL CONDUCT AUTHORITY |

| MEMBER OF THE LONDON STOCK EXCHANGE |

| NOT FOR DISTRIBUTION IN THE U.S.A. |

This factsheet has been issued by Fiske plc on the basis of publicly available information, internally developed data and other sources believed to be reliable and accurate. No representations or warranty, expressed or implied, is made nor responsibility of any kind is accepted by Fiske plc, its directors or employees either as to the accuracy or completeness of any information stated in this factsheet. Any opinions expressed (including estimates and forecasts) may be subject to change without notice. This document is not intended as an offer to buy or sell the fund nor as a personal recommendation. Fiske plc, or any of its connected or affiliated companies or their employees, may have a position or holding or other material interest in the fund concerned or in a related investment, or may have provided within the previous twelve months, significant advice or investment services in relation to the investment concerned or a related investment.

Investors must be aware of the risks associated with investment in this fund. Full details of the Atlas Global Equity Income Fund, including risk warnings, are published in the Prospectus and Key Investor Information Document (KIID). The fund may not be suitable for all investors and if you are in any doubt whether the fund is suitable for you, advice should be sought from a suitably qualified professional advisor. The value of the fund and the income derived from it can go down as well as up. Investors may not get back their initial investment. Past performance is not necessarily a guide to future performance. Estimates of future performance are based on assumptions that may not be realised. Securities denominated in foreign currencies may see their value fall as a result of exchange rate movements. Any comments contained in this factsheet are intended only for the use of the individual or entity to which it is addressed and may contain information which is confidential and may also be legally privileged. If you have received this document in error, please telephone the Compliance Department on +44 (0)20 7448 4700. Fiske plc FCA Register No: 124279