Atlas Global Equity Income – Monthly Manager Commentary

May 2026

During May we introduced new positions in Infineon Technologies and US defence contractor Lockheed Martin. At the same time we took some profits and reduced our exposure to Games Workshop following a well-received trading update. We also took some profits in ASML and Siemens Energy following strong performance.

Featured holding – Infineon Technologies

Infineon Technologies has been manufacturing semiconductors as an independent company for 27 years, but its history in this arena goes back much further. The business was Siemens AG’s dedicated semiconductor division before being spun out as Infineon Technologies AG in 1999 and subsequently listed via an initial public offering (IPO).

Driven by the artificial intelligence (AI) boom, Infineon is now experiencing significant growth in its data centre division and from its power semiconductor products. This growth is led by its flagship OptiMOS™ silicon semiconductors and highly integrated vertical power modules, which have become the industry standard for delivering clean, high-density power directly to graphics processing units (GPUs) and advanced AI accelerators.

History

Infineon Technologies listed on the German stock market in March 2000, at a time when the dot-com bubble was at its peak. The IPO was 33 times oversubscribed. The stock price doubled on its first day of trading, to €70 per share from an IPO price of €35, but for the next two years it dropped relentlessly, reaching approximately €6 per share by December 2002.

Back in 2000 Infineon manufactured computer memory chips (DRAM), which made up 48% of revenue. The company also produced wireless and wireline communication semiconductors, automotive microcontrollers for vehicle electronics and power integrated circuits (ICs) for industrial management systems.

Infineon eventually exited its DRAM memory business by spinning it off into a wholly owned subsidiary named Qimonda AG in 2006. The aim was to shield its core business from severe volatility in the memory market and refocus on the more stable markets for automotive and industrial chips. Qimonda subsequently went public through an IPO on the New York Stock Exchange, with Infineon initially retaining a majority stake. However, due to falling memory prices, Qimonda ultimately filed for insolvency in 2009.

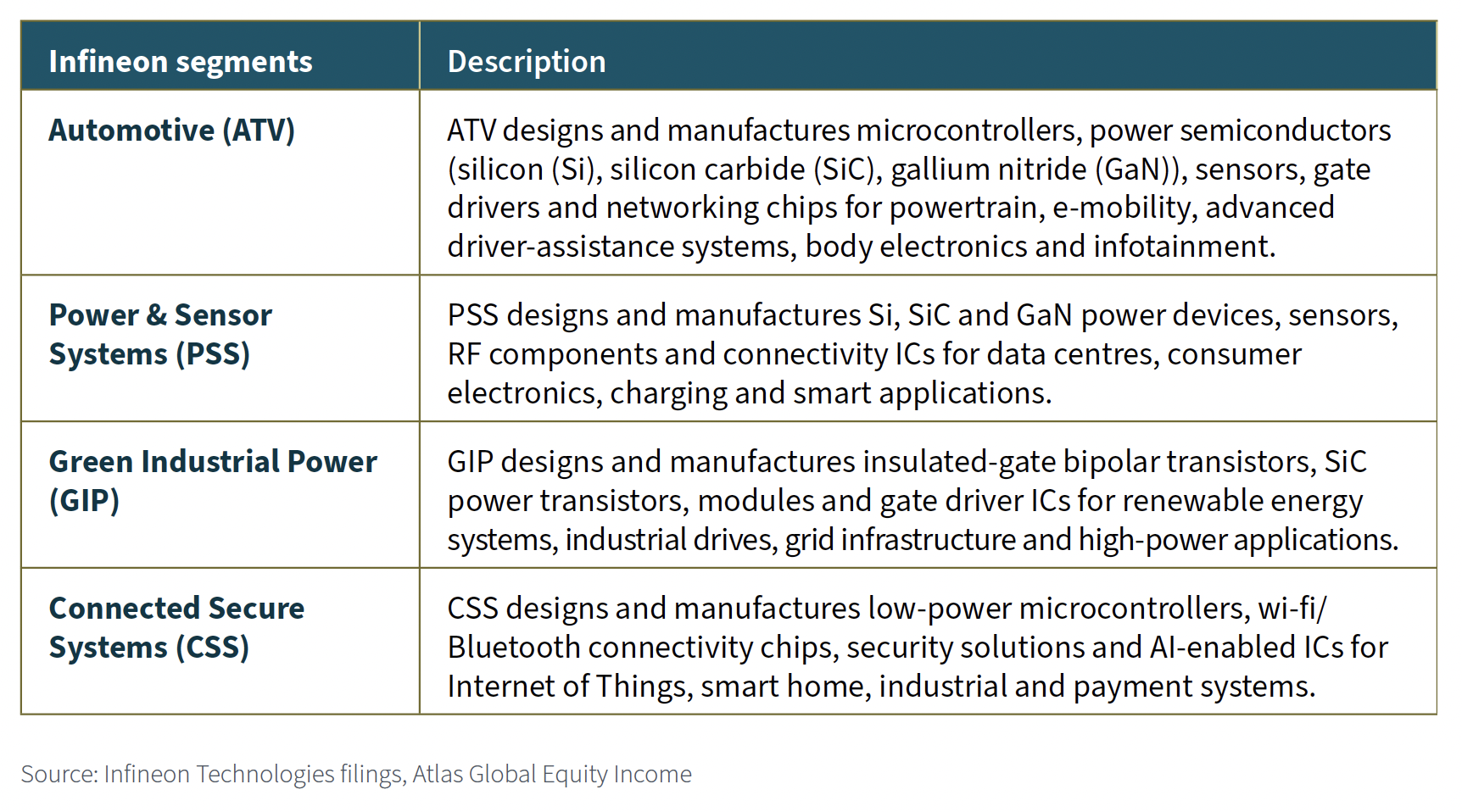

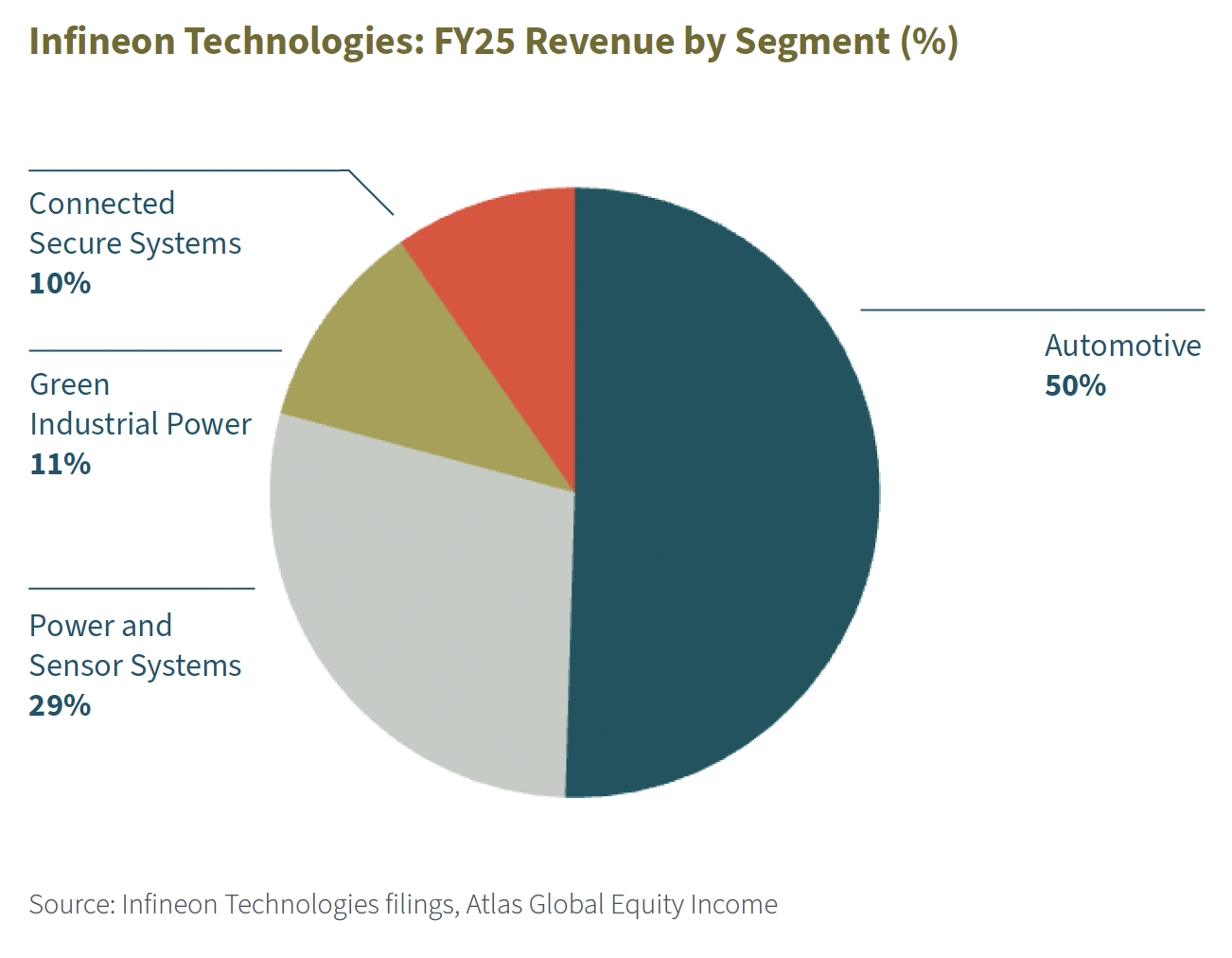

FY25 sector exposure – by revenue

Infineon Technologies reported total revenue of €14.7 billion for FY25. Its Automotive (ATV) division led the way, contributing €7.4 billion, with the remaining revenue split between Power & Sensor Systems (PSS – €4.2 billion), Green Industrial Power (GIP – €1.6 billion) and Connected Secure Systems (CSS – €1.4 billion).

Following a period of inventory buildup by automakers in response to the COVID-19 pandemic, Infineon’s ATV division suffered significant inventory corrections that dragged on throughout 2024 and 2025. The sector now appears to have stabilised, showing improved order intake and long-term demand for software-defined vehicles.

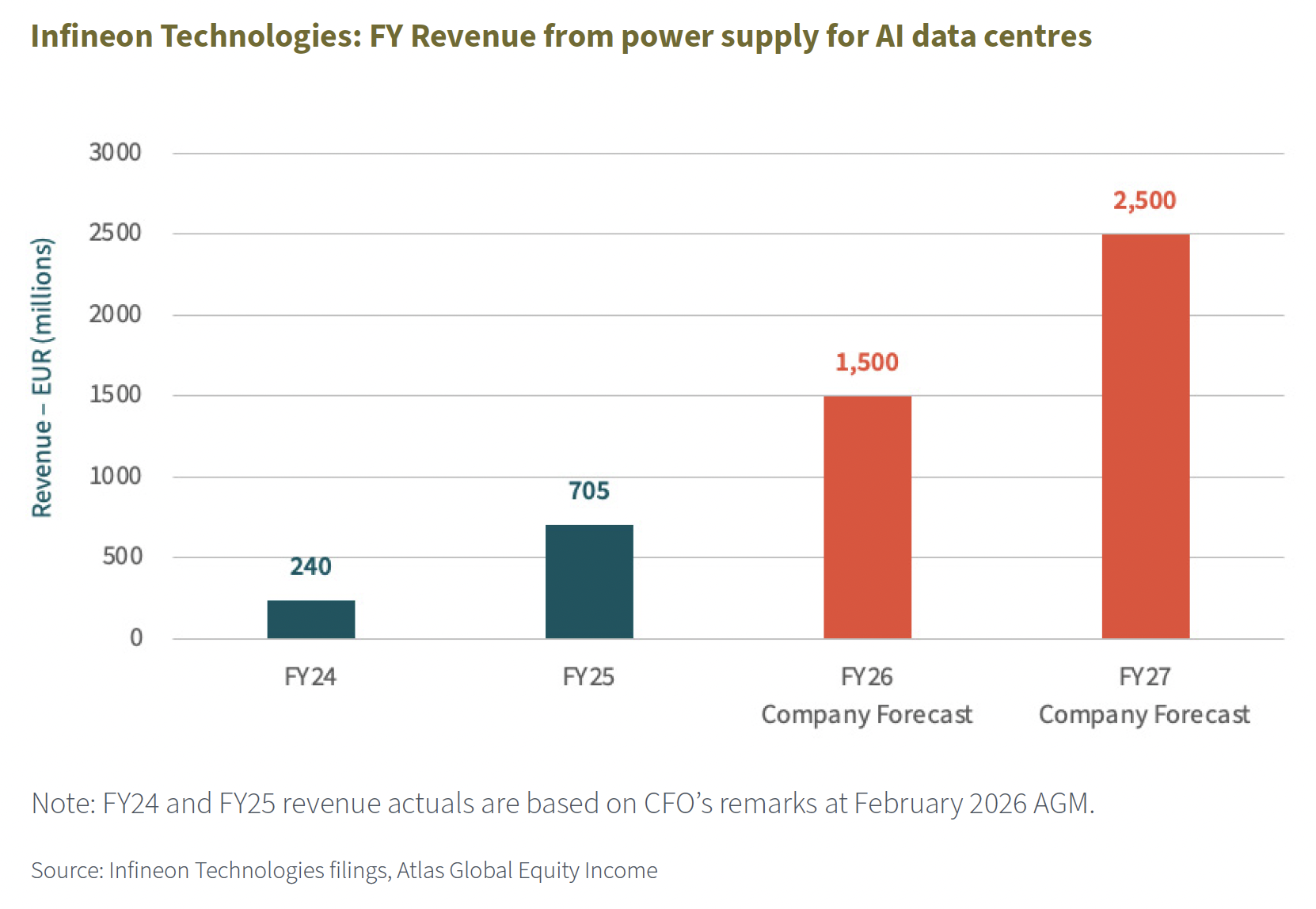

However, it is within the PSS segment that significant growth is appearing. Speaking at the company’s AGM in February 2026, CFO Dr Sven Schneider identified the key growth driver as power supply for AI data centres, noting: “In this application area we nearly tripled our revenue to more than €700 million. This is around €100 million more than forecast, despite negative currency effects.”

In May this year, discussing the company’s prospects for the rest of 2026, CEO Jochen Hanebeck said: “In the second half we will grow more strongly than previously expected, with a broader upcycle across many end markets now in sight. The AI boom strengthens further, and our power supply solutions for AI data centres are in very high demand. The expansion of power infrastructure is gaining momentum and is becoming an increasingly important growth driver for our industrial business.”

Speaking during Infineon’s Q2 2026 earnings call, Hanebeck added: “Currently, our AI business is on allocation. We are converting capacities from other areas, as well as ramping new ones as quickly as possible. Given the unabated momentum, we are reconfirming our guidance of dedicated AI power revenues of €1.5 billion for 2026, as well as our indication of €2.5 billion for 2027, irrespective of a weaker US dollar.”

So what kinds of “power supply solutions for AI data centres” does Infineon offer?

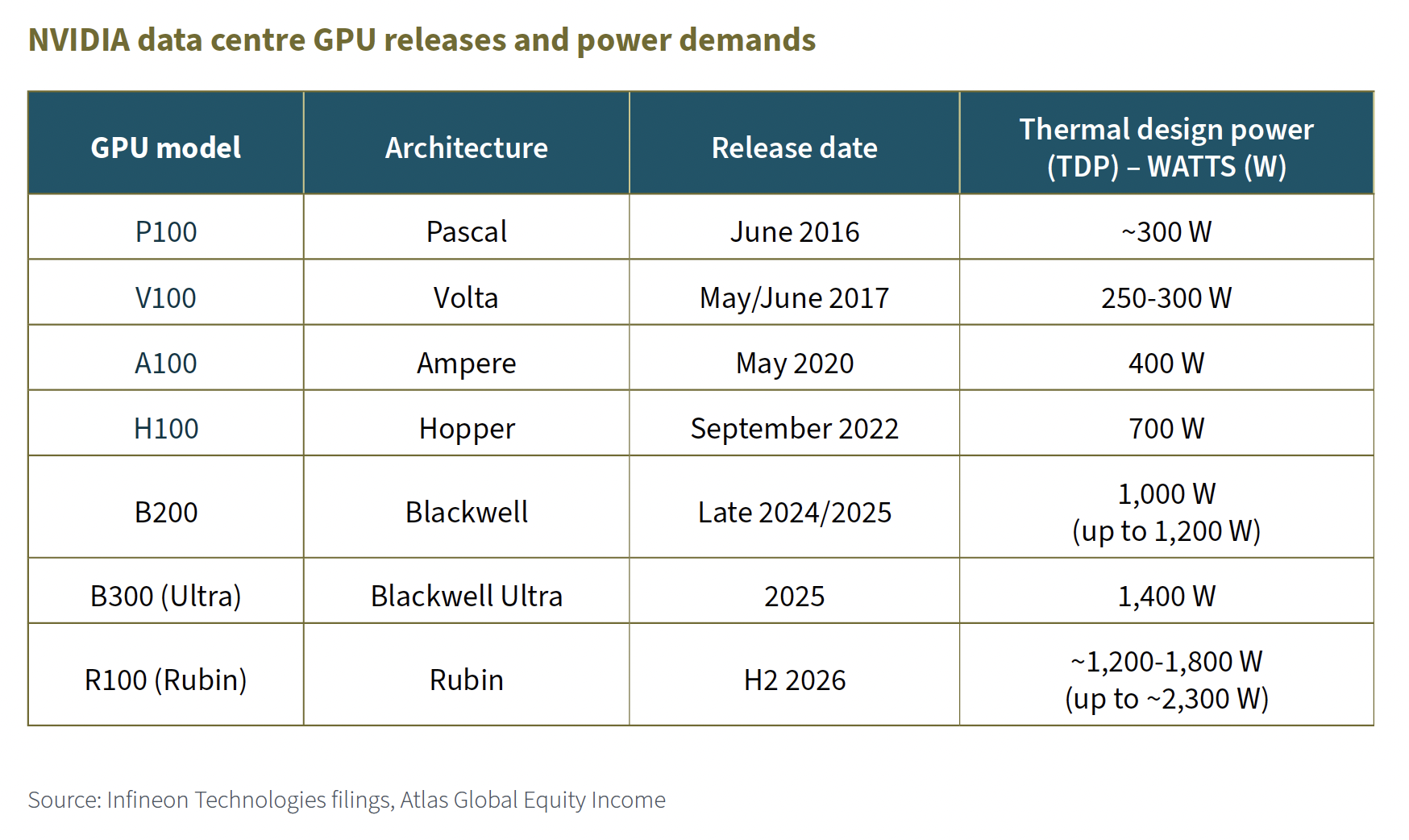

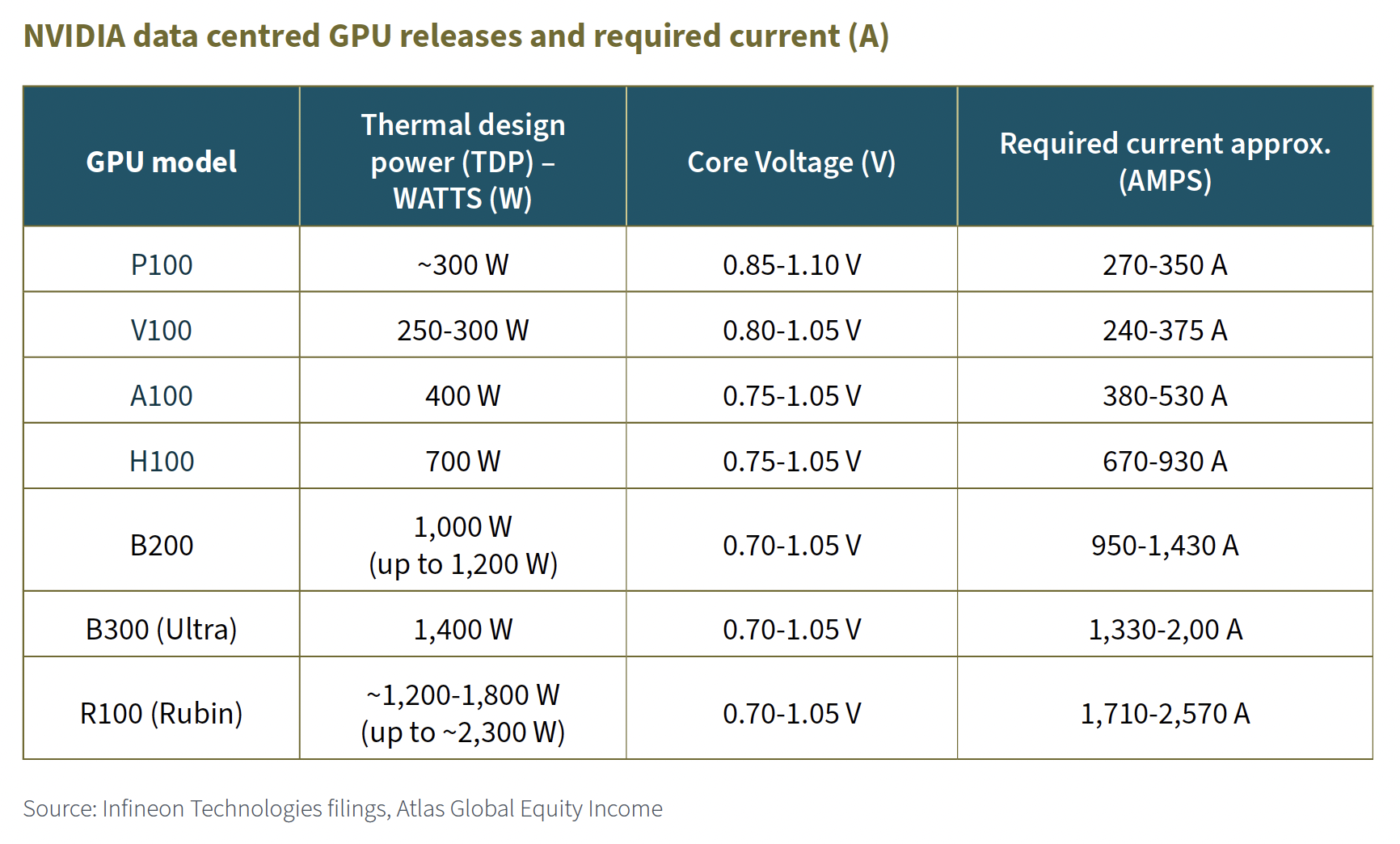

Before we answer this, let us take a look at the increasing power demands of data centre equipment – specifically, those of the Nvidia GPUs used over the past 10 years. The right-hand column in the table below shows the power requirement for each model. Notice the significant increase as these GPUs crunch more and more data.

The problem

GPUs and other types of accelerator processors need to receive voltages of around 1 volt or lower. Higher voltages would destroy the thin insulating layers on the transistors, and the transistors would literally melt – a process known as hard dielectric breakdown.

As you may remember from physics classes at school, electrical engineers are constrained by the formula below. If they want to increase power but voltage cannot be increased then they need to increase the current.

The table below shows the current in amps needed for each GPU model in order to provide the necessary power. Notice the significant increase in current from the P100, released in 2016, to the R100, which is expected in the second half of 2026.

Crucially, increasing current has implications in the form of power loss. Think of all those electrons moving through the copper wires on the circuit board. The wires themselves have a natural resistance of their own, and power is lost as heat.

To compound the issue, notice the power loss formula. Power loss increases by current squared – which means, for example, that doubling the current increases power loss fourfold! These losses become an acute problem near the point at which voltages are stepped down to around 1 volt and current increases dramatically.

The solution

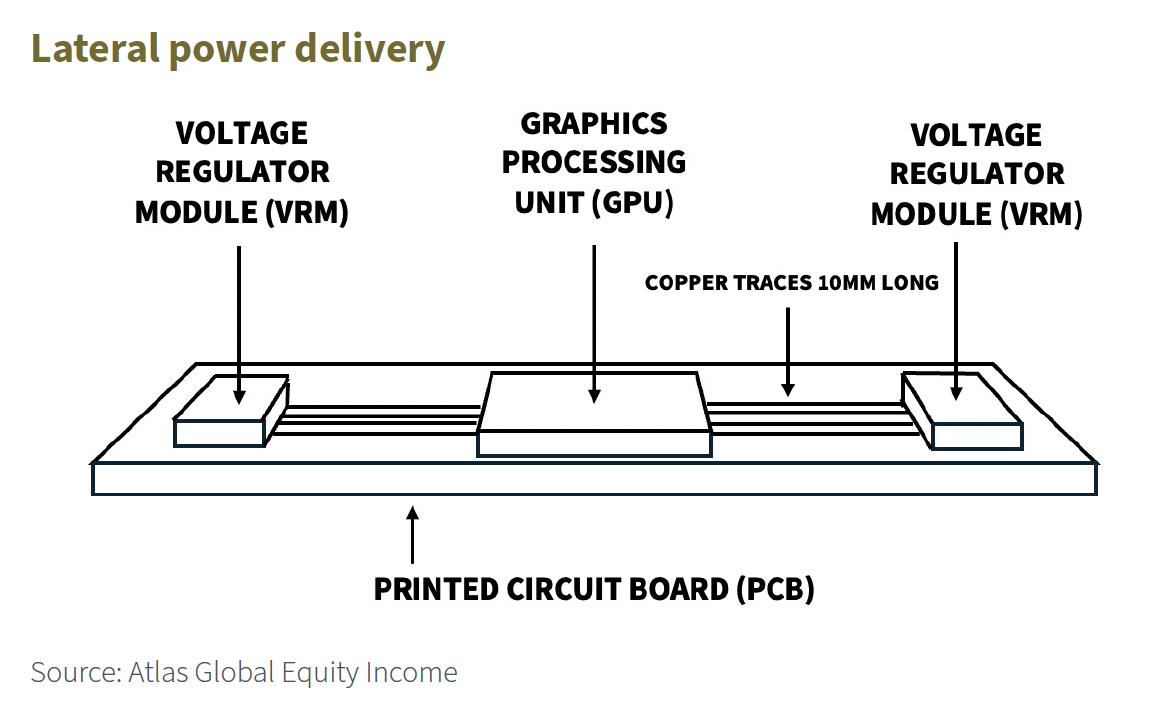

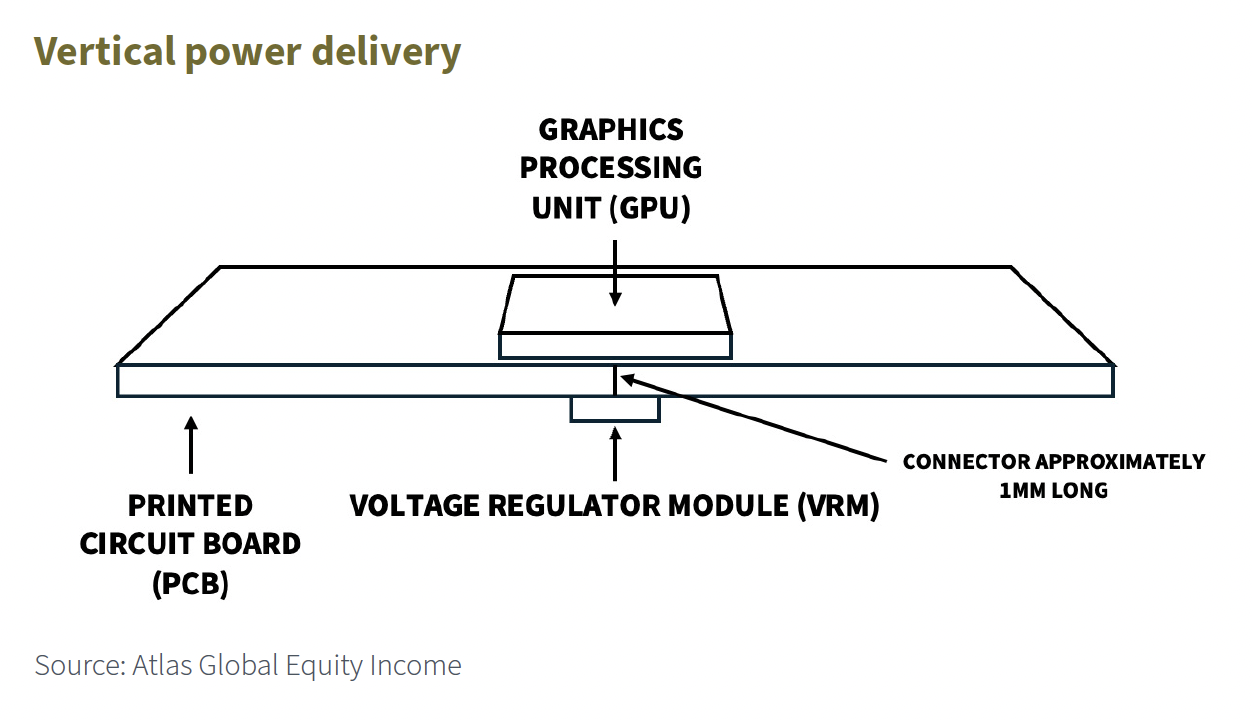

Historically, power has been delivered to a GPU by voltage regulator modules (VRMs) located to the side of the GPU. The power is then delivered through copper traces. This setup is known as lateral power delivery.

This was suitable for P100 processors from a decade ago, when the current was about 350 amps at most. But the upcoming R100 (Rubin) processor will need this to increase around seven times, to about 2,500 amps. Power losses – which, as mentioned, increase by current squared – will be 49 times higher!

This is where vertical power delivery (VPD) comes in. If voltages need to be around 1 volt and current needs to go up to maintain the power delivery, the only way to reduce power losses is to reduce resistance. VPD does this by cutting the length of the copper traces.

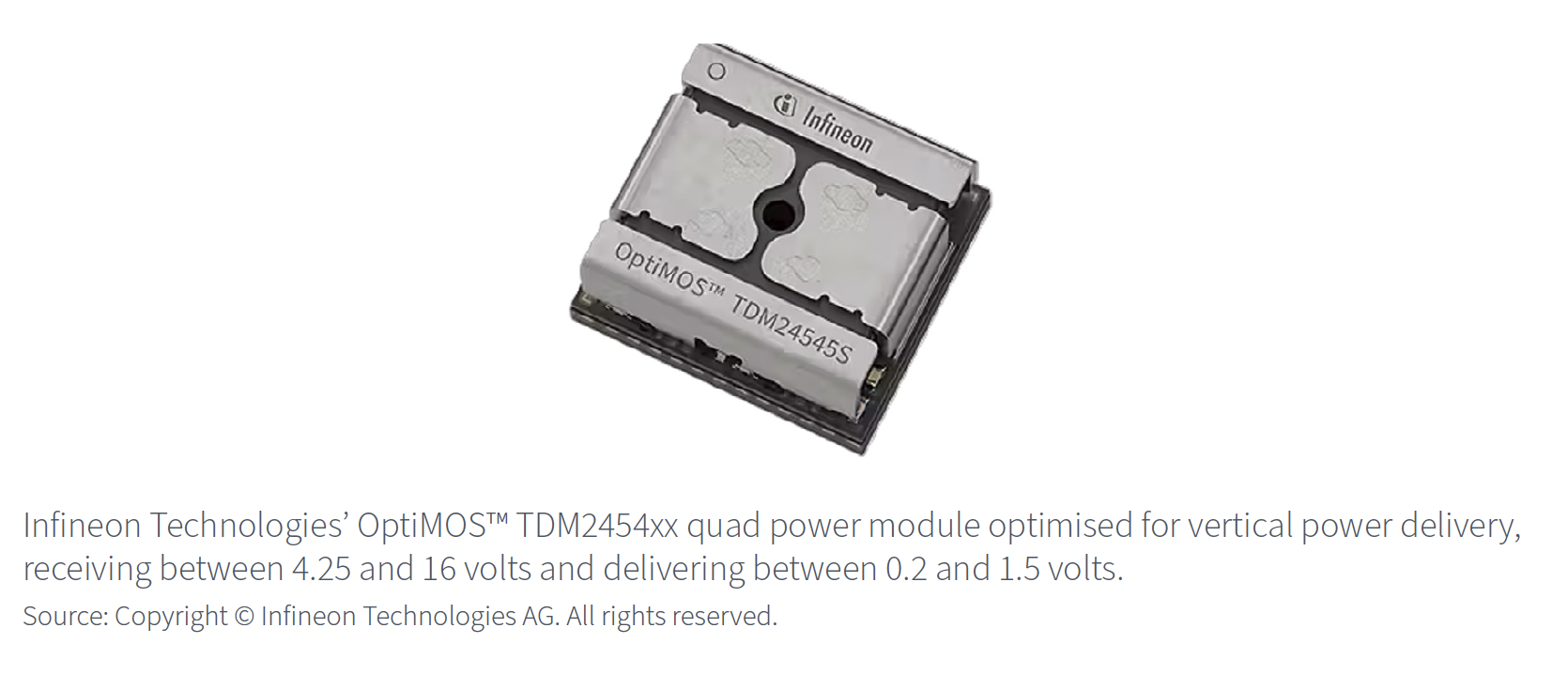

Infineon has been working on this issue. Its OptiMOS™ TDM2454xx is an integrated power module designed to deliver large, efficient currents to high-performance computing chips in AI data centres. It enables vertical power delivery by minimising the physical distance that power travels, significantly reducing resistive energy loss.

The module contains 12 silicon trench N-channel MOSFETs (using Infineon’s OptiMOS 6 technology) embedded directly into the substrate. These transistors provide the robust switching and thermal efficiency required to support massive power loads in a highly compact form factor.

The OptiMOS™ TDM2454xx delivers market-leading current density exceeding 2 amps/mm². This capability is critical, as high-bandwidth memory (HBM) crowds a GPU’s topside perimeter, leaving no room for traditional regulators. Mounting this ultra-dense module directly to the underside of a printed circuit board (PCB) bypasses the layout conflict, cutting power delivery path lengths and ultimately lowering resistive losses.

Conclusion

Infineon Technologies is well-positioned to benefit from the strong growth in AI data centres. Its OptiMOS™ VPD solutions, such as the TDM2454xx, are already delivering major efficiency gains for today’s high-power AI GPUs and are fully qualified for next-generation platforms such as Nvidia’s upcoming Rubin.

Importantly, power delivery for GPUs is just one part of Infineon’s portfolio. Looking ahead, the company is playing a leading role in the shift to 800-volt DC power architectures for future AI server racks. Working with Nvidia, it is using CoolSiC™ and CoolGaN™ technologies to support high-voltage direct current distribution. This approach reduces power losses, improves rack density and helps enable large multi-megawatt AI clusters.

Separately, Infineon’s portfolio of power semiconductors, microcontrollers, sensors and motor control solutions is supporting the development of advanced robotics and humanoid systems. These products provide the compact, energy-efficient performance needed for precise motion control and actuation.

With AI infrastructure, high-voltage power systems and robotics converging, Infineon’s innovation pipeline and diversified portfolio position the company for continued leadership and long-term growth.

Disclaimer:

As at the end of May 2026, Atlas Global Equity Income holds a long position in Infineon Technologies.

This article is not to be taken as investment advice.

Michael Foster, Fund Manager and Roger Breuer, Analyst – Atlas Global Equity Income

May 2026

………………………

| AUTHORISED AND REGULATED BY THE FINANCIAL CONDUCT AUTHORITY |

| MEMBER OF THE LONDON STOCK EXCHANGE |

| NOT FOR DISTRIBUTION IN THE U.S.A. |

This factsheet has been issued by Fiske plc on the basis of publicly available information, internally developed data and other sources believed to be reliable and accurate. No representations or warranty, expressed or implied, is made nor responsibility of any kind is accepted by Fiske plc, its directors or employees either as to the accuracy or completeness of any information stated in this factsheet. Any opinions expressed (including estimates and forecasts) may be subject to change without notice. This document is not intended as an offer to buy or sell the fund nor as a personal recommendation. Fiske plc, or any of its connected or affiliated companies or their employees, may have a position or holding or other material interest in the fund concerned or in a related investment, or may have provided within the previous twelve months, significant advice or investment services in relation to the investment concerned or a related investment.

Investors must be aware of the risks associated with investment in this fund. Full details of the Atlas Global Equity Income Fund, including risk warnings, are published in the Prospectus and Key Investor Information Document (KIID). The fund may not be suitable for all investors and if you are in any doubt whether the fund is suitable for you, advice should be sought from a suitably qualified professional advisor. The value of the fund and the income derived from it can go down as well as up. Investors may not get back their initial investment. Past performance is not necessarily a guide to future performance. Estimates of future performance are based on assumptions that may not be realised. Securities denominated in foreign currencies may see their value fall as a result of exchange rate movements. Any comments contained in this factsheet are intended only for the use of the individual or entity to which it is addressed and may contain information which is confidential and may also be legally privileged. If you have received this document in error, please telephone the Compliance Department on +44 (0)20 7448 4700. Fiske plc FCA Register No: 124279