Atlas Global Equity Income – Monthly Manager Commentary

June 2026

During June we introduced a small new position in Lumentum. Following strong share price performance, we took some profits and reduced our exposure to Diploma and Texas Instruments. We also took some profits from SK Hynix following a period of strong performance.

Featured holding – Lam Research

To some people, “plasma” sounds like a fictional substance from 1980s sci-fi movies. Remember Ghostbusters, where characters fired concentrated plasma from “proton packs” to trap ghosts?

Well, plasma is real. In simple terms, it is a super-hot, electrically charged gas that has found a critical use in advanced semiconductor manufacture. Often described as the fourth state of matter, it is the next step in thermal transformation.

We all know that heating ice melts it into liquid water. Similarly, we all know that boiling water vaporises it into gas. In turn, exposing gas to extreme temperatures strips away electrons to create plasma.

Consider a neon light: when switched on, a surge of high voltage transforms the internal gas into a glowing plasma of energetic electrons and positive ions, producing its signature vibrant radiance.

The origins of Lam Research

A critical step in silicon chip manufacture involves removing photoresist material once it is no longer required. In the 1950s and early 1960s this relied entirely on a liquid-based process known as wet stripping.

Technicians would submerge silicon wafers in heated baths of volatile organic solvents or highly corrosive acids, such as sulfuric acid blended with hydrogen peroxide. The process was sufficient for the transistor sizes manufactured at the time, but it was hazardous for cleanroom operators, generated toxic waste and lacked precision.

Signetics, one of the first Silicon Valley companies dedicated exclusively to making integrated circuits, developed a dry stripping approach in 1968. This removed photoresist by using an oxygen plasma. The method took place within a sealed chamber, protecting operators from toxic chemicals while using significantly smaller amounts of chemical agents. It was a major leap forward.

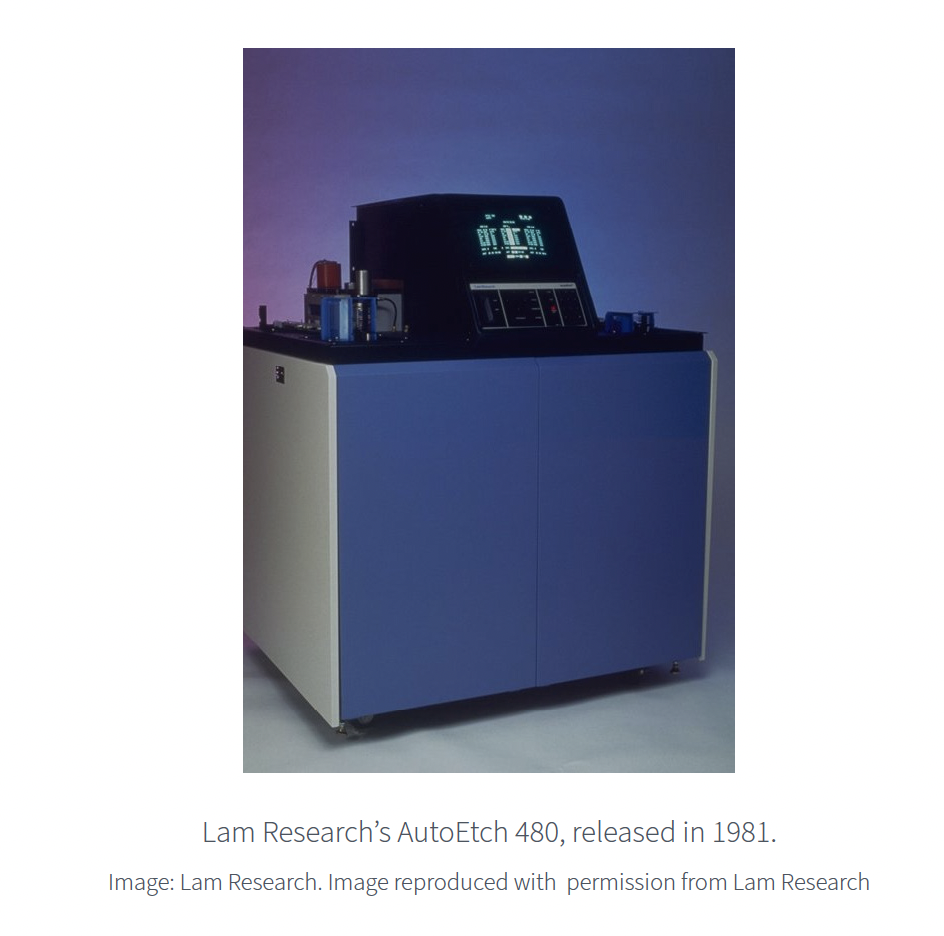

The origins of Lam Research go back to these early days of dry stripping. In the 1970s, while working on plasma systems at Texas Instruments and Hewlett-Packard, David Lam observed that a process known as dry etching worked well in R&D labs but struggled in production. Manual, analogue controls led to massive process variability, as operators frequently made unauthorised and inconsistent adjustments to the delicate chemical environments.

As chips shrank and transistors became microscopic, this human error became unacceptable. Lam realised that smaller features required extreme precision and repeatability. He saw that automating the plasma process by using digital control was the only way to eliminate human variability – paving the way for his groundbreaking, fully automated AutoEtch system.

In 1980 Lam mortgaged his home and secured initial funding from angel investors, including Intel co-founder Bob Noyce. This financial backing allowed him to establish Lam Research in Silicon Valley and bring his idea to life.

Novellus acquisition

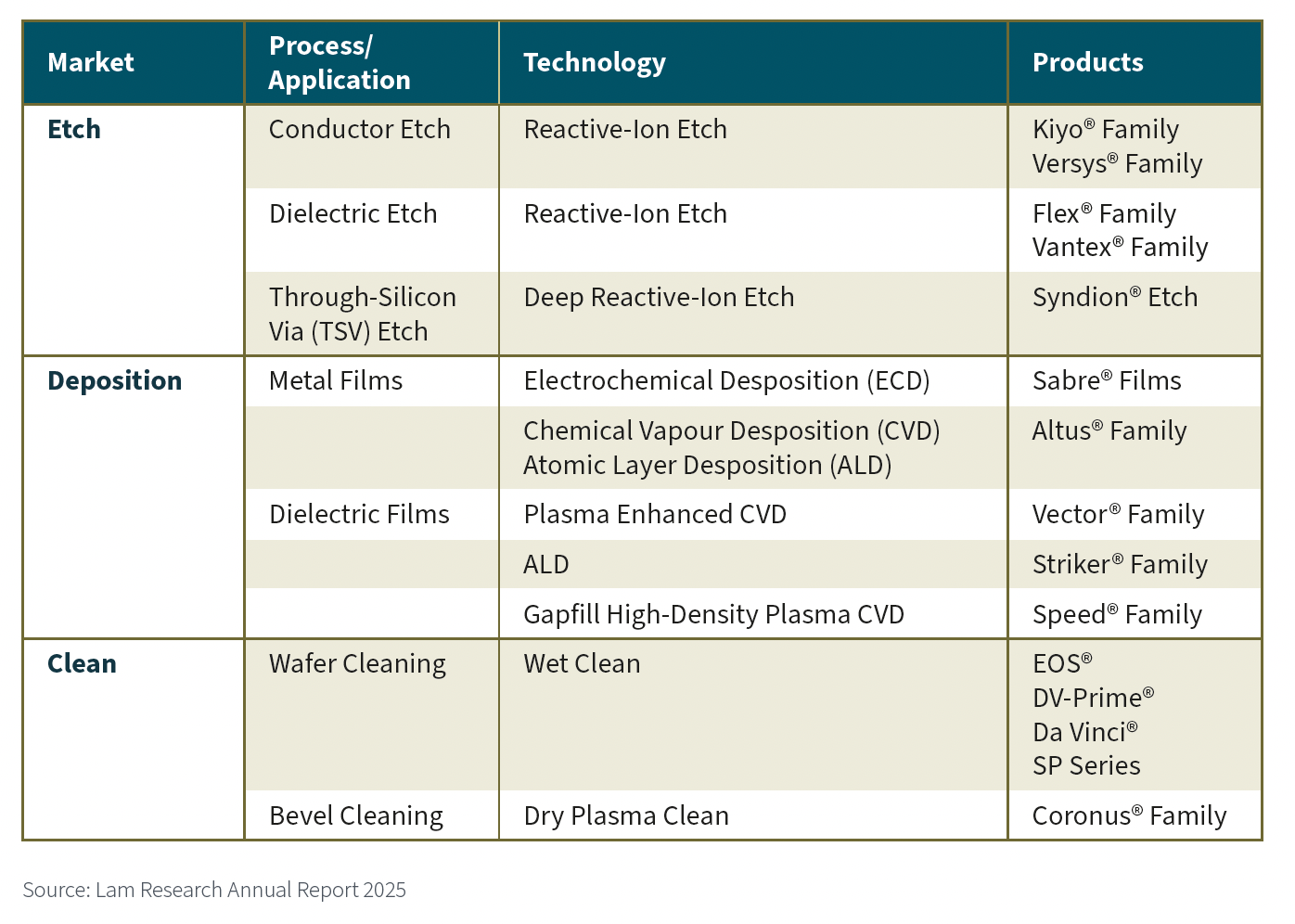

Lam Research was originally known as a focused specialist rather than a diversified tool supplier. Its engineering expertise and market dominance were highly concentrated in two specific phases of wafer processing: etching (removing materials to create microscopic patterns) and cleaning (washing away residue and impurities from the wafer between manufacturing steps).

Because the company lacked its own material deposition technology, chipmakers had to use a Lam tool to etch a trench and then move the wafer to a machine built by a competitor – for example, Applied Materials or Novellus Systems – to deposit the metal or dielectric film inside that trench.

In 2011 Lam bought Novellus Systems for $3.3 billion, adding critical deposition technology to its existing etch-and-clean portfolio. This strategic transaction successfully integrated adjacent manufacturing steps, transforming Lam into a full-suite supplier of front-end equipment for advanced semiconductor wafer manufacture.

The table below shows the full suite of Lam Research machines across the etch, deposition and clean stages, as offered at year end June 30 2025.

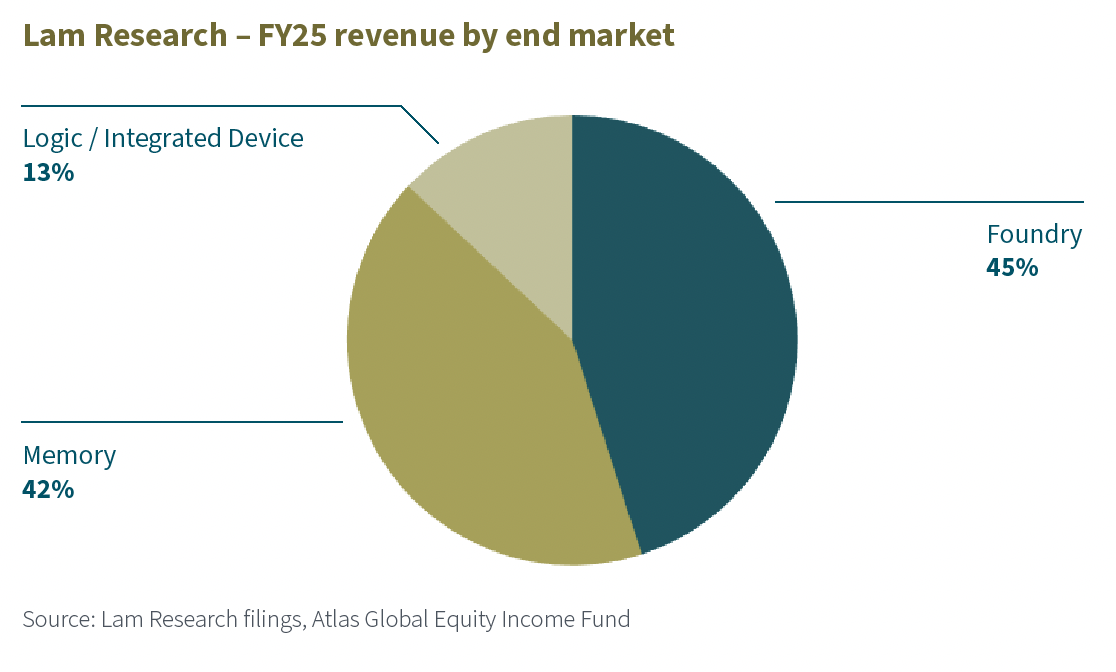

The chart below shows Lam’s FY25 revenue by end market. Notice the strong exposure to memory.

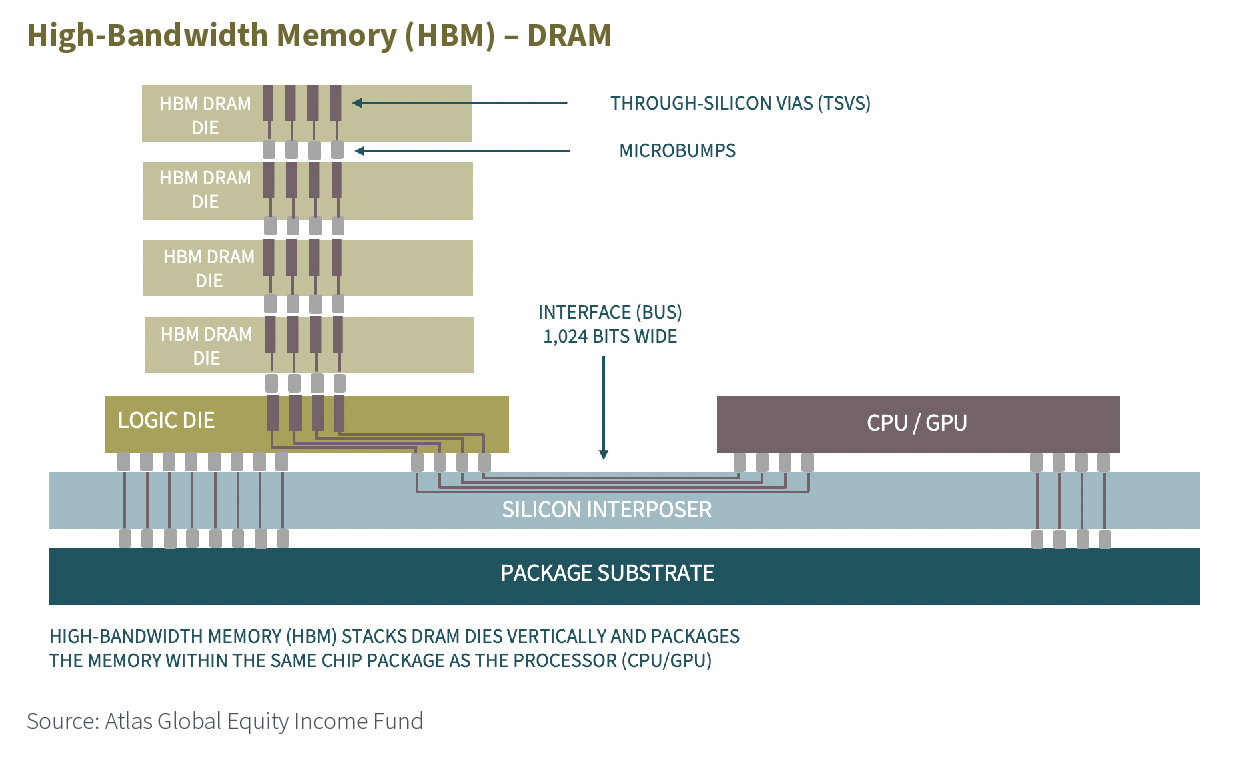

Artificial intelligence (AI) workloads require vast amounts of data to train and execute algorithms without processor delays. To eliminate this bottleneck, accelerators rely on high-bandwidth memory (HBM). By vertically stacking dynamic random-access memory (DRAM) dies directly beside a graphics processing unit (GPU), HBM dramatically reduces latency and delivers massive data throughput.

HBM manufacturing – which is currently controlled by an oligopoly of SK Hynix, Samsung and Micron – has some key technical challenges. The image below shows the stacked die formation of HBM, with electrical connectivity using through-silicon vias (TSVs) – tiny holes etched through the silicon and filled with copper to make the electrical connection.

Etching these precise, uniform holes through silicon dies at a microscopic scale requires specialised equipment capable of overcoming severe physical constraints. As HBM stacks grow taller, manufacturers must etch increasingly narrow channels with extremely high aspect ratios.

To meet this challenge, Lam developed the Syndion® product platform – the company’s deep reactive-ion etching (DRIE) tool. Syndion® is engineered to control plasma uniformity at the wafer level, carving perfectly straight, vertical channels with atomic-scale precision. By ensuring these microscopic holes are uniform from top to bottom, Lam’s technology provides the foundational, defect-free electrical pathways needed to reliably connect the stacked DRAM dies in modern HBM architectures.

Following the etching process, Lam’s Striker® atomic layer deposition (ALD) platform deposits uniform dielectric liners into the narrow TSVs, shielding the channels against electrical leakage. Next, the Sabre® 3D electrochemical deposition system fills these insulated pathways with copper, ensuring void-free filling and perfectly aligned microbumps for dense die stacking.

Ultimately, Lam’s Syndion, Striker and Sabre 3D platforms deliver the critical etching, insulation and metallisation technologies required to build the high-density, defect-free TSV connections that power modern HBM architectures.

These machines are why Lam has such significant exposure to the memory industry.

Installed base

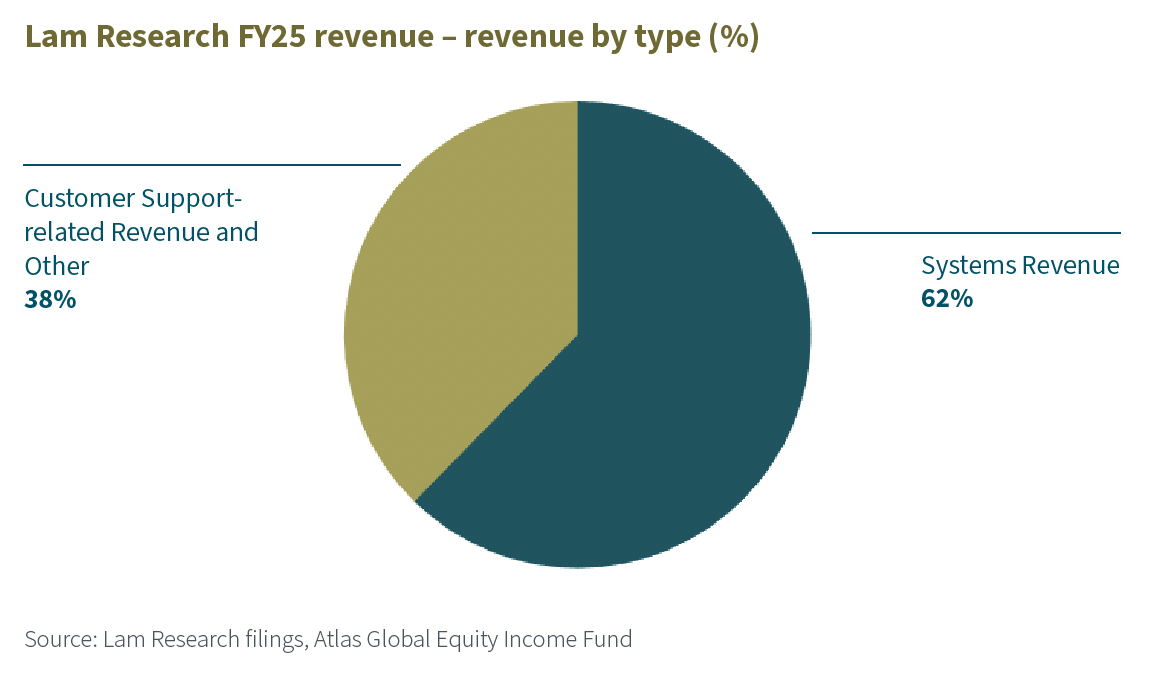

Lam Research’s global installed base, which scaled to nearly 100,000 active process chambers in FY25, serves as a massive foundation for predictable recurring income. Of Lam’s record $18.4 billion FY25 revenue, the Customer Support Business Group generated $7 billion from aftermarket supplies, upgrades and services, complementing the $11.4 billion brought in by primary chipmaking equipment sales.

Conclusion

Lam Research’s decades of specialised expertise in etch, deposition and clean equipment position it well for the growth of the semiconductor industry. Through the 2011 acquisition of Novellus, the company became a full-suite supplier of front-end wafer-processing tools. This makes Lam a critical “picks and shovels” provider for the AI boom, particularly via its support for HBM manufacturing. The Syndion platform’s deep reactive-ion etching creates uniform high-aspect-ratio TSVs, complemented by Striker atomic layer deposition for dielectric liners and Sabre 3D electrochemical deposition for void-free copper filling.

Lam’s near-100,000 installed process chambers provide a strong base for recurring revenue, with the Customer Support Business Group delivering $7 billion of the company’s $18.4 billion FY25 revenue.

In our view, with decades of pioneering history in semiconductor manufacturing and a strong reputation built on delivering high-quality equipment, Lam Research stands as a trusted market leader that is ready for the industry’s next era of growth.

Disclaimer:

As at the end of June 2026, Atlas Global Equity Income holds a long position in Lam Research.

This article is not to be taken as investment advice.

Michael Foster, Fund Manager and Roger Breuer, Analyst – Atlas Global Equity Income

June 2026

………………………

| AUTHORISED AND REGULATED BY THE FINANCIAL CONDUCT AUTHORITY |

| MEMBER OF THE LONDON STOCK EXCHANGE |

| NOT FOR DISTRIBUTION IN THE U.S.A. |

This factsheet has been issued by Fiske plc on the basis of publicly available information, internally developed data and other sources believed to be reliable and accurate. No representations or warranty, expressed or implied, is made nor responsibility of any kind is accepted by Fiske plc, its directors or employees either as to the accuracy or completeness of any information stated in this factsheet. Any opinions expressed (including estimates and forecasts) may be subject to change without notice. This document is not intended as an offer to buy or sell the fund nor as a personal recommendation. Fiske plc, or any of its connected or affiliated companies or their employees, may have a position or holding or other material interest in the fund concerned or in a related investment, or may have provided within the previous twelve months, significant advice or investment services in relation to the investment concerned or a related investment.

Investors must be aware of the risks associated with investment in this fund. Full details of the Atlas Global Equity Income Fund, including risk warnings, are published in the Prospectus and Key Investor Information Document (KIID). The fund may not be suitable for all investors and if you are in any doubt whether the fund is suitable for you, advice should be sought from a suitably qualified professional advisor. The value of the fund and the income derived from it can go down as well as up. Investors may not get back their initial investment. Past performance is not necessarily a guide to future performance. Estimates of future performance are based on assumptions that may not be realised. Securities denominated in foreign currencies may see their value fall as a result of exchange rate movements. Any comments contained in this factsheet are intended only for the use of the individual or entity to which it is addressed and may contain information which is confidential and may also be legally privileged. If you have received this document in error, please telephone the Compliance Department on +44 (0)20 7448 4700. Fiske plc FCA Register No: 124279