Atlas Global Equity Income – Monthly Manager Commentary

March 2026

During March we initiated a new position in SK Hynix, the global leader in high-bandwidth memory (HBM) semiconductors. We also took profits and reduced our holding in Siemens Energy following its strong share price performance over recent months. In addition, we fully exited our position in Visa due to growing concerns over potential antitrust action by the Department of Justice regarding the company’s dominant position in payment transactions.

Featured holding – Gaztransport et Technigaz

The name Gaztransport et Technigaz does feel a bit clunky. It is the direct result of a 1994 merger between Gaztransport and Technigaz, two pioneering French engineering firms. Both companies specialise in developing membrane containment systems for liquefied natural gas (LNG) carriers, and the merger combined their rival technologies.

Even for those who are not fluent in French, the name is fairly intuitive. “Gaz” is not too far from “gas”, and “transport” is self-explanatory. From this point on, nonetheless, we will refer to the company as GTT.

What really interests us about GTT is its extraordinarily high returns on investment – over 54%

in 2024, as measured by HOLT’s Cash Flow Return on Investment – which is underpinned by a near-monopoly position in membrane containment technology for LNG carriers and related applications.

Investment returns – Cash Flow Return on Investment (CFROI)

![]()

Liquefied natural gas containment systems

Before we look closer at the company, what are liquefied natural gas (LNG) containment systems?

Natural gas, which is mostly methane with small amounts of ethane and propane, is commonly transported by pipeline. This works well locally but becomes unfeasible when transporting across oceans and between continents. This is where liquefying natural gas, by cooling it to approximately -162ºC, is useful. The process shrinks its volume by roughly 600 times, making it more practical to store and transport long distances by ship. It costs a huge amount to build the equipment to refrigerate the natural gas into liquid, but the economics work at large enough scale.

Once the natural gas is in liquid form, the trick is to prevent it from turning back into gas. LNG containment systems are the highly insulated tanks on ships (or storage facilities) which keep the LNG cold and therefore in liquid form. They usually have a thin metal barrier to hold the liquid, thick insulation to keep heat out and often a second backup barrier in case the first leaks. There are two main LNG containment system types: Moss-type and membrane.

Moss-type design

Moss-type LNG carriers are named after Moss Maritime, the Norwegian company that designed and patented the spherical tank system in the early 1970s. Moss pioneered this independent, self-supporting aluminium sphere design for safe, reliable LNG containment (see image below).

This design was dominant from the 1970s until the mid-1990s, at which point GTT’s Mark III membrane system was introduced. By the late1990s / early 2000s, driven largely by superior space efficiency, membrane technology overtook Moss-type design.

While the Moss spherical design leaves a lot of space unused, simply lining the hull of a similar-length tanker with GTT’s membrane technology allows larger amounts of LNG to be transported. This space efficiency is a primary reason why membrane systems now dominate new, large LNG carrier orders – despite Moss-type designs having worked reliably for decades.

The LNG tanker LNG Rivers. This is a Moss-type LNG carrier with a capacity of 135,00 cubic metres (m3). Image: Pline / CC BY-SA 3.0

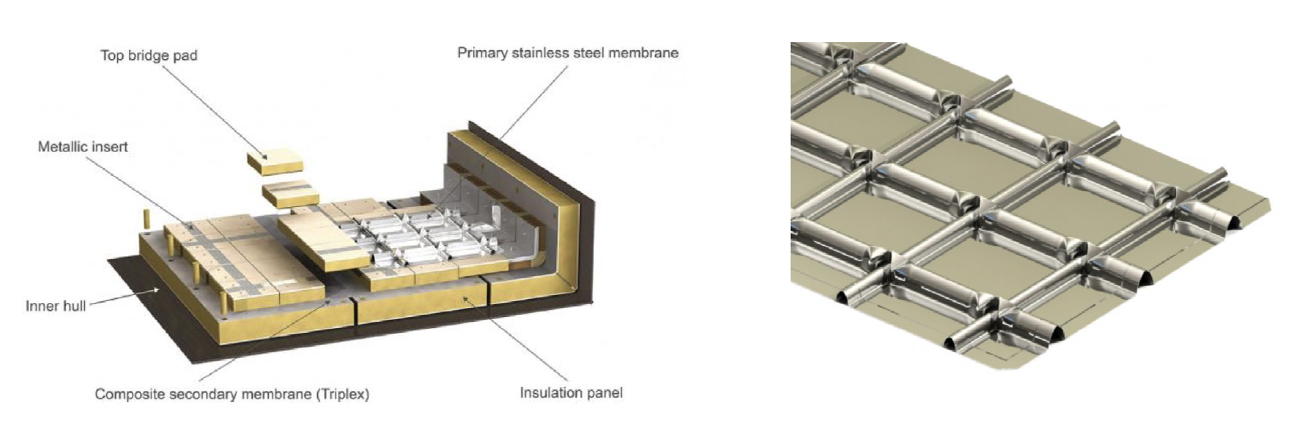

GTT’s membrane technology – Mark III

GTT’s dominant membrane technology for LNG at atmospheric pressure is known as Mark III.

It uses a primary corrugated stainless-steel membrane on top of reinforced polyurethane foam insulation panels, with a composite secondary barrier for full redundancy and safety. It can fit neatly around the inner hull of a tanker.

Left: the design of the Mark III membrane system. Right: a close-up of the primary stainless-steel membrane. Images: © GTT

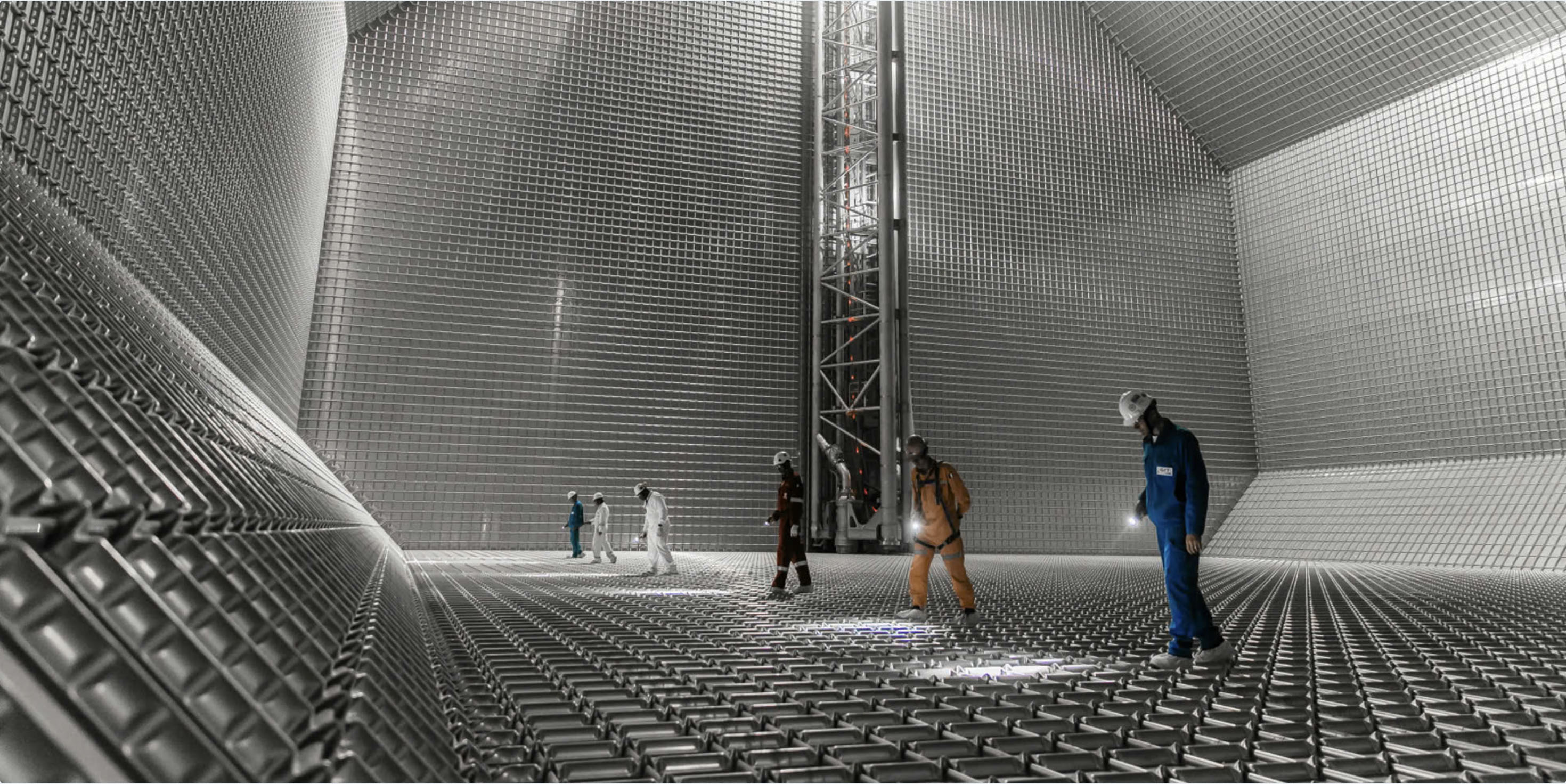

The inside of an LNG tanker once the primary stainless-steel membrane has been installed. Image: © Roland Mouron – GTT

GTT’s membrane technology – NO96

GTT has a second family of membrane technology, known as NO96. This uses a double invar (nickel-iron alloy for low thermal expansion) containment system, with two thin metallic barriers and independent insulation layers.

Boil-off rate

Boil-off rate (BOR) for LNG is the percentage of cargo volume that evaporates daily into gas due to heat getting into the cryogenic tanks. LNG stays liquid at -162°C, but any heat can cause the liquid to boil – turning liquid into gas again.

This gas needs managing – it cannot just be vented into the atmosphere. Sometimes, if suitably equipped, a tanker can use the gas as fuel. An alternative strategy is to re-liquefy the gas, but this requires more equipment on a vessel. Lower BORs reduce losses and boost efficiency on long voyages.

Typical modern BORs are 0.07-0.15% per day. GTT’s Mark III Flex+ achieves a guaranteed 0.07% per day (for ~170,000 m³ carriers using thicker insulation), while NO96 Super+ guarantees 0.085% per day (for 174,000 m³ carriers, although this can be lower on larger vessels).

The chart below shows the GTT membrane technology selected in the order book as at December 31 2024.

![]()

The Flex Rainbow LNG carrier, with a capacity of 174,000 m3. This tanker has been fitted with GTT’s Mark III Flex membrane system. Image: © GTT

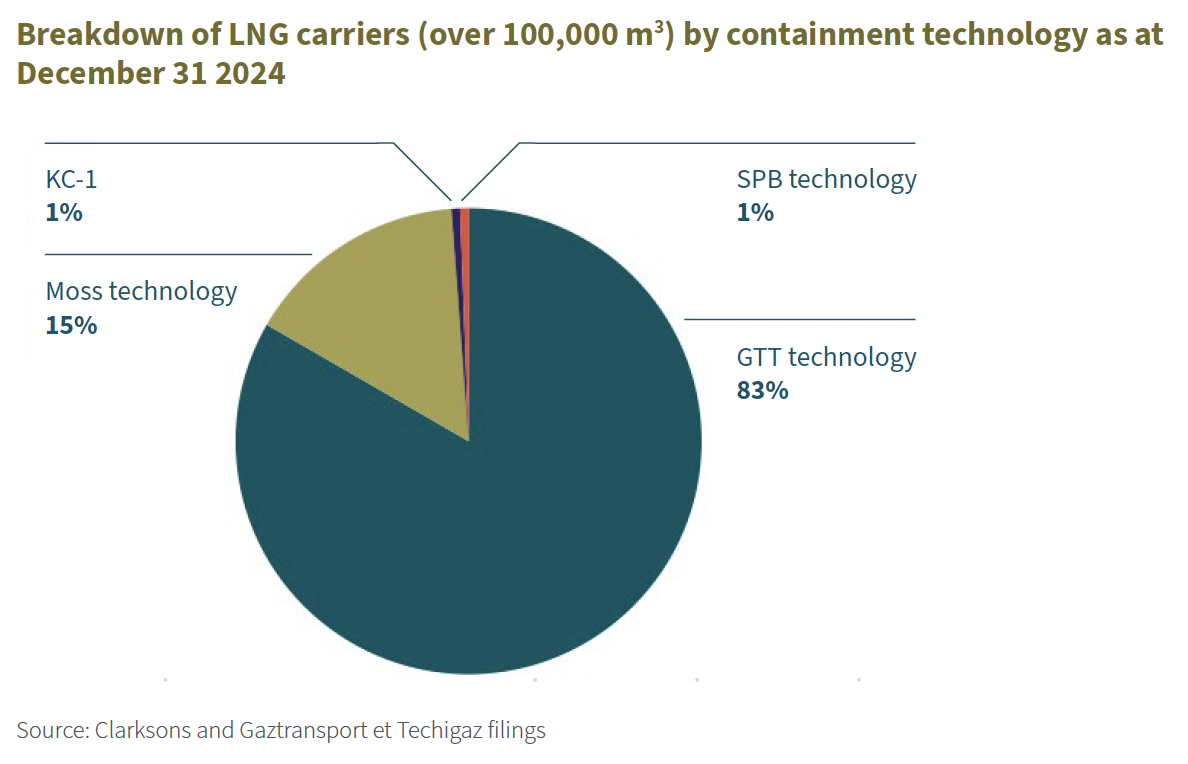

As at December 31 2024, according to GTT, 682 LNG carriers with a capacity of over 100,000 m3 were in operation globally. Of these, 565 (83%) were equipped with GTT technology.

Of course, these carriers include some old tankers. If we focus on the period between 2015 to 2024, of the 578 large LNG carriers ordered worldwide, 566 (98%) use or will use GTT containment systems.

Revenue recognition

GTT makes money from licensing its technology to shipyards, but how do the contracts work and when do they get paid? The royalty received is based on the capacity of tanker reservoirs under construction. GTT does not provide absolute value amounts for each contract, but our reading suggests each GTT contract would equate to approximately 3-5% of the construction cost of a new tanker. Typically, a modern, dual-fuel-design LNG tanker with a capacity of 174,000-180,000 m3 can cost between €220 million and €240 million. At the time of writing, due to limited shipyard capacity, these prices are facing upward pressure.

If we take the midpoint of these ranges for simplicity, the contract value for an LNG tanker with a capacity of 174,000-180,000 m3 would be approximately €9.2million.

The royalty is received not in one go but over the period of construction of the vessel, which would be approximately three years (or longer for some larger builds).

According to GTT’s annual report, the invoices are issued according to a contractual schedule based on the key phases of construction:

1. Effective date of the contract (10% of contract)

2. Steel-cutting (20% of contract)

3. Keel-laying (20% of contract)

4. Launch (20% of contract)

5. Delivery (30% of contract)

This schedule helps us understand when cash flow is received. From an accounting perspective, under IFRS, revenue is recognised over time. If a tanker is expected to take three years to build, GTT will take the contract amount, divide it by 36 months (e.g. €9.2million / 36 months = €0.255million) and recognise €0.255million each month, as revenue, irrespective of when the cash is received.

This difference between the timing of “revenue recognition” and “cash flow” explains why GTT tends to have sizeable amounts of “Other Contract Liabilities” on its balance sheet. This number includes “Contract Liabilities”, which is money received but not yet recognised as revenue. These liabilities are, of course, offset by large “Cash and cash equivalent” balances.

This is an appealing characteristic of GTT’s business model. It is good to receive cash upfront, and it helps explain why GTT is highly cash-generative and has a strong cash-conversion ratio.

The chart below shows the number of orders delivered (or completed) each year. It indicates the number of vessels (e.g. LNG tankers, ethane carriers, etc) incorporating GTT’s technology which shipyards have officially completed, tested and handed over to their ship-owner customers. FY25 was a record year in terms of deliveries.

![]()

FY25 was subdued in terms of new orders, with only 45. Some 165 orders were placed in FY22.

![]()

![]()

Revenue visibility

The order book of 288 units provides excellent revenue visibility for the next few years. GTT’s FY25 earnings report provides guidance on when the order book (as at December 31 2025) will be recognised as revenue by year.

![]()

With €609 million in revenue expected to be recognised in FY26, GTT needs to generate further revenue of between €131 million and €171 million to meet its FY26 revenue guidance of between €740 million and €780 million.

So far, in the first three months of FY26 alone, GTT has received 36 new orders – not far short of the 45 orders received during the whole of FY25 and on track, at this run rate, to match the record order intake of 165 in FY22.

![]()

Dividends

GTT has a track record of paying dividends to shareholders and has paid dividends every year since listing on the stock exchange in February 2014. These are paid twice a year and target a payout ratio of around 80% of consolidated net income.

The total dividend announced for FY25 of €8.94 implies a 4.4% trailing dividend yield at the time of writing.

![]()

Conclusion

GTT is an asset-light company that generates high returns on investment (54% Cash Flow Return on Investment as measured by HOLT). These high returns are underpinned by a near-monopoly position in LNG containment technology. The order backlog, while below recent highs, remains at elevated levels, and the start of 2026 has seen an increase in order completion compared to the first quarter of last year.

Adding to its appeal, GTT exhibits excellent revenue visibility, strong cash-conversion characteristics and a robust net cash balance sheet, which supports generous dividend payouts.

The recent war in Iran will renew discussions about energy security. The transportation of LNG is likely to play a continued role in the energy mix of nation states.

Michael Foster, Fund Manager and Roger Breuer, Analyst – Atlas Global Equity Income

March 2026

Disclaimer:

As at the end of March 2026, Atlas Global Equity Income holds a long position in Gaztransport et Technigaz (GTT).

This article is not to be taken as investment advice.

………………………

| AUTHORISED AND REGULATED BY THE FINANCIAL CONDUCT AUTHORITY |

| MEMBER OF THE LONDON STOCK EXCHANGE |

| NOT FOR DISTRIBUTION IN THE U.S.A. |

This factsheet has been issued by Fiske plc on the basis of publicly available information, internally developed data and other sources believed to be reliable and accurate. No representations or warranty, expressed or implied, is made nor responsibility of any kind is accepted by Fiske plc, its directors or employees either as to the accuracy or completeness of any information stated in this factsheet. Any opinions expressed (including estimates and forecasts) may be subject to change without notice. This document is not intended as an offer to buy or sell the fund nor as a personal recommendation. Fiske plc, or any of its connected or affiliated companies or their employees, may have a position or holding or other material interest in the fund concerned or in a related investment, or may have provided within the previous twelve months, significant advice or investment services in relation to the investment concerned or a related investment.

Investors must be aware of the risks associated with investment in this fund. Full details of the Atlas Global Equity Income Fund, including risk warnings, are published in the Prospectus and Key Investor Information Document (KIID). The fund may not be suitable for all investors and if you are in any doubt whether the fund is suitable for you, advice should be sought from a suitably qualified professional advisor. The value of the fund and the income derived from it can go down as well as up. Investors may not get back their initial investment. Past performance is not necessarily a guide to future performance. Estimates of future performance are based on assumptions that may not be realised. Securities denominated in foreign currencies may see their value fall as a result of exchange rate movements. Any comments contained in this factsheet are intended only for the use of the individual or entity to which it is addressed and may contain information which is confidential and may also be legally privileged. If you have received this document in error, please telephone the Compliance Department on +44 (0)20 7448 4700. Fiske plc FCA Register No: 124279